Ambiq’s IPO is good fun, and 7 Q2 '25 VC data points

And: Why Core Scientific shareholders are upset over the CoreWeave deal

Welcome to Cautious Optimism, a newsletter on tech, business, and power.

Tuesday! If you are interested in venture happenings, Sequoia’s Shaun Maguire’s social media posts concerning the Israel-Hamas war and the Democratic nominee for Mayor of New York City has attracted criticism. Some retorts have been humorous, but now several hundred founders, investors, and technology denizens have banded together, calling for the venture firm to apologize. That won’t happen — but the letter is a reminder that the technology industry truly is global, with constituent members of all creeds and perspectives.

In news less likely to generate discourse, Waymo is heading to Philadelphia and New York City for testing. And, I hope, commercial launches in time. More cities, faster, please! — Alex

📈 Trending Up: AI voice scams … market disregard for tariff threats … no, really … flooding in Tibet … “vegetarian rocket engines” … history rhyming … EV sales in China … NATO drones … farm tensions in trade deals … generative games … 16.34 million TEUs … Boldstart Ventures …

📉 Trending Down: Crypto data privacy … domestic bond dominance in China? … global press freedom … telecos + media … global shipping safety … AI rule delays in the EU … African venture capital …

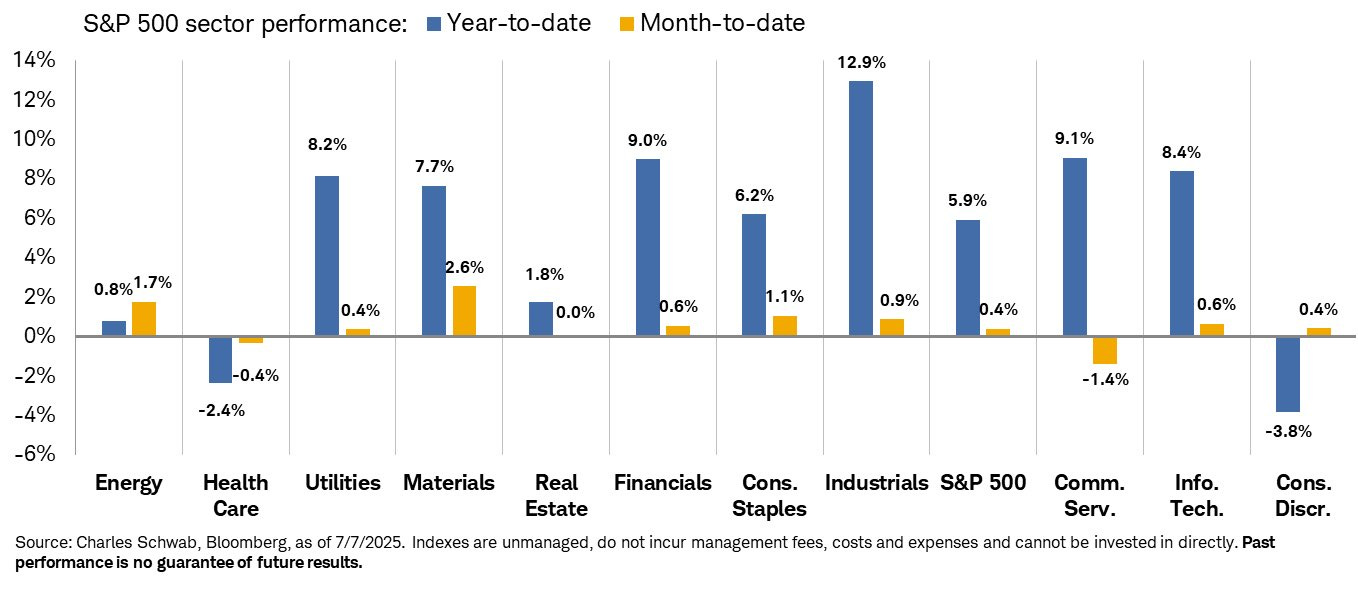

📊Chart(s) of the Day:

Why Core Scientific shareholders are upset over the CoreWeave deal

Yesterday, news that CoreWeave will buy Core Scientific for $9 billion was the headline of the morning. However, despite offering what was described as a stiff premium to Core Scientific’s pre-deal share price, investors promptly dumped the smaller company’s stock.

CoreWeave will pay 0.1235 of its shares for every share of Core Scientific, which it calculates is worth “$20.40 per share value based on the closing price of CoreWeave Class A common stock as of July 3, 2025, and a premium of approximately 66% to the unaffected Core Scientific closing share price of $12.30 on June 25, 2025.”

Following the news, Core Scientific’s stock collapsed from around $18 per share to just under $15 this morning. What’s going on? Why would Core Scientific investors ditch their shares if CoreWeave is offering such a sweet deal?

Because the transaction is a set equity exchange, not a set value exchange. In simple terms: If CoreWeave loses value between now and when the deal closes, then the effective value of the transaction will fall (the dollar value of the shares that CoreWeave pays out). Or as the deal memo put it: “The final value will be determined at the time of transaction close.”

So: Core Scientific investors saw the deal, looked at the equity exchange rate, considered whether or not CoreWeave is overvalued today, and hit the escape button. They are wagering that CoreWeave will lose value between now and when its Core Scientific takeover completes, making the deal worth less than the headline $9 billion figure.

With a price/sales ratio of over 27x, CoreWeave certainly isn’t cheap today.

Ambiq’s IPO is good fun!

It’s common today to go public very late, waiting for a startup to become worth enough at debut to become an instant candidate for S&P500 inclusion. That $20.5 billion minimum doesn’t guarantee inclusion — just ask Robinhood — but the threshold underscores just how big tech companies are getting while private.

There are outliers, however, willing to brave the public markets earlier in their maturity cycle. Ambiq is one such company. The Texas-based low-power semiconductor company builds System-on-Chip (SoC) products for edge AI use cases. In English that means Ambiq makes chips for AI compute for devices like smartwatches, medical hardware, and industrial IoT.

While we tend to think of AI compute in units of datacenter-gigawatts, it’s worth recalling that not every device has a fiber connection to a remote compute installation. Sometimes you’ll need to parse the data locally, and that’s where Ambiq steps in.

Don’t write off IoT — Samsara has been crushing it in recent years.

Ambiq is at first look an unimpressive company. Here’s its income statement:

As you can see, Ambiq grew 16% last year, while reducing its net losses. But while the company did make some improvements to its operating results last year, to kick off 2025, Ambiq grew just 3.4%, and made only modest progress against its preceding year’s Q1 loss.

What makes Ambiq interesting is that it’s been doing incredibly hard work behind the scenes to entirely dispose of its mainland China business:

[H]istorically, our sales were significantly concentrated with end customers in Mainland China. For example, in 2023, 66% of our net sales were to end customers in Mainland China, as compared to 50% in 2024. Given geopolitical concerns, subsidized competitors creating a price sensitive environment in Mainland China and our desire to service market segments outside of consumer wearable products, we have focused our management and sales efforts toward other critical geographies.

Putting the shift in more recent terms, Ambiq generated 50% of its sales in China during Q1 2024. In Q1 2025 that number was just 6%. Ambiq therefore completely ripped, and replaced its mainland China business in a single year. From that perspective, Ambiq crushed its last four quarters.

Even more, leaving the Chinese market with its subsidized competition greatly boosted Ambiq’s gross margins:

Returning to where we started, Ambiq could have waited another year to go public — in theory, we don’t have all the details. By doing so, it could have wrapped its China exit and put more points on the board concerning its ability to sell in other markets. Instead, here we are, looking at a company that at first glance is a bit blah, but under the hood could be building something big for our collective AI future. Fun!

China’s government has been making noise in recent weeks about lowering internal-market price competition as it looks to avoid persistent deflation. The Ambiq exit from China hinging on subsidized local competition in that market is further evidence that state-led industrial policy is hard to execute without enormous market distortion.

7 Q2 2025 VC data points

Pulling from the PitchBook/NVCA + global first-look dataset:

US-based startups raised $69.9 billion in Q2 2025, just under 70% of the global total of $101.5 billion in the quarter.

European startups raised 13% less in Q2 2025 compared to Q1 2025, with both counted and expected deal volume also falling.

Exit value of $67.7 billion for US startups was the best quarterly result since 2021. Thus, this is the post-ZIRP exit high. Enjoy!

Through Q2 2025, AI investments in the United States were worth 64.1% of total deal value, and 35.6% of total deal volume. Those figures are up from both 2023 and 2024.

The world is less AI-focused, with just 53% of venture deal value through the second quarter heading to AI shops, along with 29% of deal count.

US pre-seed and seed deal value was $5.5 billion in the second quarter, the strongest single-quarter result since Q3 2022.

Median US pre-money valuations for pre-seed ($8.0M in 2025) and seed ($15.5M) are the highest yearly totals on record.

The above confirms what we suspected: Exits were up in Q2, early-stage deals are getting more expensive, the US venture market is incredibly AI-heavy, and the European startup flywheel could use a nudge.